Unveiling Tax-Free Settlements: What You Need to Know

Learn the complexities of what makes settlements taxable vs. non-taxable, several strategies to minimize settlement tax liabilities.

What Types of Legal Settlements are Not Taxable?

Settlements and their tax implications can often seem complex for individuals and businesses. It’s essential to grasp the nuances involving taxation of settlements to make informed decisions and reduce tax burdens.

This article dives into the details of taxation of settlements, offering insights into compensatory damages and punitive damages, as well as how different settlement types, like whistleblower settlements, are treated for tax purposes. This article also discusses strategies for minimizing tax responsibilities on settlements and answers common questions such as how to report settlement funds to the IRS and determining the portion of a taxable settlement.

Differentiating Taxable Income From Taxable Settlements

Per Section 61 of the Internal Revenue Code (IRC), all income is generally taxable unless explicitly exempted by another section of the IRC. The taxation of settlements hinges on the nature of the claim and the damages awarded.

Understanding Settlement Taxation

The taxability of settlements is contingent upon “the origin of the claim,” meaning the cause of action that led to the settlement award. Here’s a breakdown illustrating how typical settlements are taxed:

When determining the taxability of a settlement, consider these key factors:

- What was the settlement intended to replace?

- Is there a specific exemption in the tax code that applies?

The Role of IRC Section 104 – Physical Injury

IRC Section 104 excludes certain settlements and awards from taxable income. Specifically, §104(a)(2) of the IRC allows taxpayers to exclude from gross income “the amount of any damages (other than punitive damages) received on account of personal physical injuries or physical sickness.”

However, there are some important nuances to keep in mind:

- The injury must be physical in nature.

- Punitive damages are generally taxable, even if they relate to a physical injury, with a narrow exception for certain wrongful death cases.

Before 1996, Section 104(a)(2) did not have the “physical” requirement. The Small Business Job Protection Act of 1996 changed the code to restrict exclusions for injuries and sickness.

PRO TIP: Emotional distress alone does not qualify for the exclusion under §104(a)(2) unless it originates from a physical injury or sickness.

PRO TIP: Attorney fees that come with damages cannot be deducted by the plaintiff. So, the plaintiff will need to pay taxes on the amount of the award. (Refer to the discussion on strategies in the Plaintiff Recovery Trust to avoid this “double tax” situation.)

PRO TIP: Taxpayers must show that their settlement qualifies for exclusion under Section 104(a)(2). The IRS will review the language in the settlement agreement and legal claims to determine tax treatment. Using precise language in both settlement agreements and court orders can strengthen a taxpayer’s case.

Common Nontaxable Settlements

Settlements stemming from physical injury or illness are generally deemed nontaxable under Internal Revenue Code (IRC) Section 104 (a)(2). These settlements compensate individuals for injuries or sickness. Let’s look at some examples.

Personal Injury Settlements

Settlements received for personal physical injuries are typically nontaxable, including compensation for:

- Dog bites and attacks

- Motor vehicle accidents resulting in physical injury

- Medical malpractice suits based on physical illness or sickness

- Premises liability cases where injury results from property neglect

- Workplace and construction injuries

- Product liability, such as defective medications causing severe harm

The critical factor is that the settlement involves physical injury or sickness. Emotional distress damages originating from a physical injury are also nontaxable.

Medical Expense Reimbursements

When a settlement includes reimbursement for expenses related to the injury, the part of the settlement designated for those expenses is usually not taxable unless those medical expenses were previously deducted by the plaintiff. If, in a prior tax year, the medical expenses were deducted and a tax benefit was provided, then that portion of the settlement may be considered income.

Wrongful Death Settlements

Similarly, settlements for death cases are generally treated as nontaxable since they are handled similarly to injury settlements from a tax perspective. These settlements compensate the surviving family members for reasons including the loss of support, the pain and suffering experienced by the deceased, medical and funeral expenses, and the loss of potential inheritance. However, there are exceptions to consider. Punitive damages in cases of wrongful death are typically subject to taxation. Moreover, any part of the settlement that reimburses expenses previously deducted by the plaintiff may be regarded as income up to the extent of any tax benefits received.

PRO TIP: Contingent attorney fees associated with punitive damages are not deductible to the plaintiff. Accordingly, the plaintiff must pay taxes on the entire amount of the punitive award. (Plaintiff recovery Trust discussion below for strategies to eliminate this “double tax”)

Carefully review the specific circumstances of each settlement to determine the appropriate tax treatment. Consulting with a tax professional can help ensure compliance with IRS regulations.

Common Types of Taxable Settlements

Some settlements are not subject to taxes; however, some require taxation. Let’s delve into some examples of these settlements in detail.

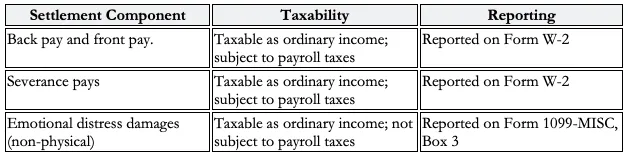

Employment Disputes and Lost Wages

Compensation received for lost wages, back pay, front pay, or severance pay is considered income and is subject to taxes, including Social Security and Medicare taxes (FICA) withholding. Here’s a breakdown of how these settlements are taxed:

It’s crucial to understand that even if some of the settlement pertains to distress damages stemming from an employment dispute, those damages remain taxable unless they result from an injury or illness.

Punitive Damages

Punitive damages are always taxable regardless of the case’s nature. These damages aim to penalize the defendant for their misconduct and do not serve as compensation for the plaintiff’s losses. Punitive damages are categorized as “Income” on Form 1099 MISC. Are taxed as ordinary income rates.

- Punitive damages are taxable even if the underlying compensatory damages are tax-free, such as in a personal physical injury case.

- The plaintiff must pay taxes on the entire gross amount of punitive damages awarded, including the portion paid to their attorney as a contingency fee.

- Punitive damages are not subject to payroll taxes, as they are not considered wages or compensation.

PRO TIP: Contingent attorney fees associated with punitive damages are not deductible to the plaintiff. Accordingly, the plaintiff must pay taxes on the entire amount of the punitive award. (Plaintiff recovery Trust discussion below for strategies to eliminate this “double tax”)

Emotional Distress Without Physical Injury

When it comes to distress without injury, payments received for mental anguish or emotional distress are usually subject to taxation unless they stem from a personal physical injury or illness. These payments may be tax-free if an injury causes emotional distress. However, these payments become taxable if emotional distress leads to symptoms like headaches or stomachaches.

Let’s consider some examples:

- Emotional distress damages arising from a non-physical injury (e.g., discrimination, defamation) are taxable.

- Emotional distress damages that cause physical symptoms but do not originate from a physical injury are taxable.

- Emotional distress damages that originate from a physical injury or sickness may be tax-free.

When receiving a settlement for emotional distress, it’s crucial to work with a tax professional to determine the appropriate tax treatment based on the specific circumstances of your case.

Whistleblower Taxation

There is no tax exemption exception for False Claims Act whistleblower awards. As such, whistleblowers must pay income taxes on their rewards at the ordinary income tax rates. As such, it remains wise to seek competent advice, as tax questions regarding whistleblower rewards are complex.

PRO TIP: Federal and state income tax burdens apply to qui tam rewards like any other form of ordinary income.

Strategies to Minimize Tax Obligations on Settlements

For those seeking to minimize settlement tax obligations, there are strategies available to reduce the taxes and maximize the recovery for plaintiffs. Utilizing settlement annuities, the Plaintiff Recovery Trust, and proper allocation in settlement agreements can help individuals reduce their tax burden and secure their future.

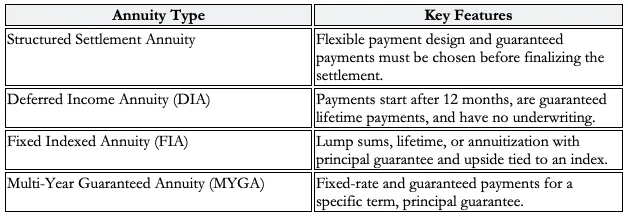

Structured Settlement Annuities

Structured settlement annuities provide a tax option for recipients of settlements by spreading out the settlement payments over several years instead of receiving a lump sum. This approach helps lower the tax rate. It offers benefits such as tax deferral, guaranteed growth of funds within the annuity, and enhanced financial stability. Regular payments can help secure your future and prevent spending decisions. Different types of annuities offer diverse features:

Plaintiff Recovery Trusts

Moreover, Plaintiff Recovery Trusts (PRTs) are tools to avoid taxation for plaintiffs receiving settlements that include attorney fees. By transferring the litigation interest to the trust, plaintiffs only pay taxes on their recovery as beneficiaries, increasing after-tax earnings by 30 to 70%.

PRTs offer additional benefits:

- Increased Premiums: PRTs can increase available structure premiums by 30% in a typical case.

- Simplified Fee Deferral: PRTs eliminate the need to match payment schedules for lawyers’ deferred fees.

- Asset Protection: PRTs can offer increased safeguarding, against creditors by operating as an entity.

Proper Allocation in Settlement Agreements

The tax implications of settlements hinge on the source and nature of the claims involved. By distributing settlement funds in the agreement, plaintiffs can optimize the portion of their recovery exempt from taxes.

- Identify Tax-Free Damages: Allocate funds to claims for personal physical injuries or physical sickness, which are generally tax-exempt under IRC Section 104(a)(2).

- Separate Punitive Damages: Allocate punitive damages separately, as they are always taxable, regardless of the underlying claim.

- Negotiate at Arm’s Length: Ensure allocations result from adversarial, good-faith negotiations to withstand IRS scrutiny.

By strategically employing structured settlement annuities, plaintiff recovery trusts, and proper allocation in settlement agreements, plaintiffs can significantly minimize their tax obligations and maximize their net recovery, providing long-term financial security and peace of mind.

Conclusion

The tax consequences associated with settlements can be complex and diverse, underscoring the importance for individuals and organizations to grasp the intricacies of taxable versus taxable settlements.

Understanding the basics of damages, punitive damages, and how settlements are taxed can help readers make informed decisions to lower their tax burden. Utilizing methods like settlement annuities, plaintiff recovery trusts, and careful allocation in settlement agreements can cut down on taxes. Increase the final amount received. It’s advisable to seek guidance from tax experts and lawyers to handle the intricacies of settlement taxation in line with IRS rules.

For a comprehensive overview of tax minimization strategies, see our guide on minimizing tax liability on lawsuit settlements.

Learn how the Plaintiff Recovery Trust addresses the attorney fee double tax created by Commissioner v. Banks.

You Have Needs,

We Have Expertise

Discover trust and settlement solutions you won’t find anywhere else – thoughtfully designed to protect assets, simplify processes, and deliver peace of mind.

Expert guidance, every step of the way.